Bank of Canada Governor Tiff Macklem expects slow economic growth and a soft labour market through the back half of the year as U.S. tariffs and uncertainty over the future of continental trade weigh on business investment and hiring in Canada.

Speaking to reporters from the annual International Monetary Fund and World Bank meetings in Washington, Mr. Macklem said he expects the Canadian economy to grow at a sluggish pace in the third and fourth quarters, and he cautioned against putting too much weight on September job numbers, which showed a rebound in employment.

“It’s going to be growth, but it’s going to be soft growth. It’s not going to feel very good, and it’s certainly not going to be enough to close the output gap,” Mr. Macklem said, noting that the bank is projecting growth in gross domestic product of around 1 per cent in the second half of the year.

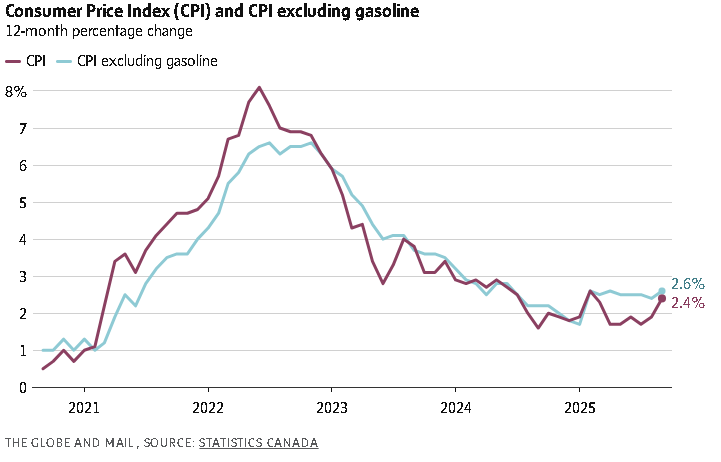

He gave no indication of whether the central bank would cut interest rates again at its meeting on Oct. 29. There are several key pieces of data still to come, he said, including September inflation numbers and the bank’s quarterly business survey, which will be published next week.

The bank lowered its policy rate to 2.5 per cent last month, the first rate cut since March. It resumed monetary policy easing after deciding that downside risks to Canada’s tariff-battered economy outweighed upside risks to inflation.

Financial markets are pricing in a roughly 80-per-cent chance of another quarter-point cut at the bank’s October meeting, according to LSEG data.

Much of the debate around the upcoming rate decision centres on how Mr. Macklem and his team are thinking about Canada’s labour market. After two months of significant job losses, employment rebounded by 60,000 in September, although the unemployment rate remained at an elevated 7.1 per cent.

Mr. Macklem suggested the bank wouldn’t put much weight on a single jobs report, given that monthly numbers can be volatile.

“Big picture, what you’re seeing in the labour market is the heavily tariffed sectors are being severely affected,” Mr. Macklem said, pointing to job losses in steel, aluminum, autos, lumber and the transportation industries that support them.

Beyond those sectors, “you’re not seeing a lot of layoffs, but you’re also not seeing a lot of hiring,” he said.

“So, if you have a job, you probably still have a job, unless you’re in one of those highly affected sectors. But you’re seeing youth unemployment is going up because new entrants into the labour market, it’s taking them longer to find a job.”

The Canadian economy contracted 1.6 per cent in the second quarter, led by a sharp pullback in exports. Mr. Macklem said he doesn’t expect another big decline in exports, “but neither are we expecting a rapid rebound.”

Business investment is likewise expected to remain weak, Mr. Macklem said, as companies remain apprehensive until they have a better sense of the Canada-U.S. trade relationship. Canadian negotiators were back in Washington this week trying to secure relief from President Donald Trump’s sector-specific tariffs, but they have not made any breakthroughs.

Both countries have also launched consultations ahead of the review of the United States-Mexico-Canada Agreement on free trade, which will happen next year.

“Uncertainty about U.S. trade policy has come down a bit since where we were in February, March, April, even July. I think uncertainty, though, is shifting now to what happens to CUSMA,” Mr. Macklem said, referring to the free-trade pact. “Until businesses have clarity on what is the outcome of that review, that is going to hold back business decisions.”

The one bright spot for the Canadian economy has been consumer spending, which remained strong through the second quarter. Mr. Macklem said he expects consumption growth to continue, but at a more moderate pace.

Canada’s central bankers will head into the next rate decision armed with a new economic forecast in the quarterly Monetary Policy Report.

Since January, the Bank of Canada has held off on publishing a central forecast, given the huge level of uncertainty around U.S. trade policy and its implications for Canada. Instead, it has published upside and downside scenarios.

“We will be using a new base-case projection to look forward,” Mr. Macklem said. “Against the background of heightened uncertainty, we will need to be humble about our forecasts, and we will continue to put a lot of emphasis on the risks.”

There’s one other key piece of uncertainty: the federal budget, which will be published on Nov. 4, only a few days after the interest rate decision. The Parliamentary Budget Officer and a number of private sector forecasters expect a big jump in Ottawa’s deficit, given increased spending on defence and infrastructure combined with weak revenue growth.

Mr. Macklem said the bank will need to see the budget before adjusting its forecasts for the Canadian economy. But he said the broad strokes of Prime Minister Mark Carney’s approach to fiscal policy are becoming clear, with plans to shrink the government’s operating budget while spending more on major infrastructure.

“When we look at the budget, we will be looking at both the demand impulse but also the potential to build the economy’s supply capacity … It’s that balance between demand and supply in the economy that we look at closely,” he said.